According to the National Association of Real Estate Investment Trusts (REIT), investors in REITs have enjoyed as much as 28 per cent returns in equity each of the last two years, and globally REIT values are up. The question is, can investors expect that same return this year?

A recovering market provides several assets to REIT investors: more dependable tenants, higher occupancy rates, and better resale property values. However, a recovering market also means, in general, higher borrowing rates.

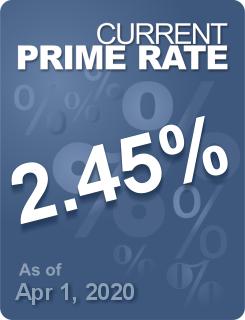

While economists are changing their prediction tune over the Bank of Canada rates announcement to be made July 19 – meaning fewer are thinking the announcement will declare a rate hike – most are still holding onto the opinion that rates will rise by December.

Continue reading “REITs Forecasted to Produce another Year of Good Returns”